EU Crypto Regulation Explained: An Essential Guide (2026)

EU crypto regulation is no longer a distant concept or a future concern. It is currently enforceable and already reshaping how crypto and fintech companies operate across the European Union.

With MiCA, the Travel Rule, and related frameworks rolling out, the EU now has one of the most comprehensive regulatory environments for crypto assets in the world.

This guide breaks down what EU crypto regulation entails, what matters most to fintech and crypto firms, and how to navigate the evolving rules.

At InnReg, we help crypto and fintech teams operationalize EU regulations, including MiCA, the Travel Rule, DORA, and PSD2/EMI, covering licensing, disclosures, and day-to-day compliance operations. If you’re planning CASP authorization or updating controls for EU rollout, contact us.

What Is EU Crypto Regulation?

EU crypto regulation refers to the set of legal and supervisory frameworks governing the operation of crypto-asset businesses across the European Union.

It includes the Markets in Crypto-Assets Regulation (MiCA), the revised Transfer of Funds Regulation (TFR), anti-money laundering directives, and several related laws that affect operational resilience and payment services.

These rules standardize how crypto businesses register, disclose information, manage risks, and interact with customers across all 27 member states. They apply to both EU-based firms and non-EU companies offering crypto services within the region.

Why EU Crypto Regulation Matters for Fintech and Crypto Startups

MiCA and related regulations apply to any business offering crypto-related services to users in the EU. That includes embedded finance platforms, neobanks, cross-border payment providers, and hybrid models that combine crypto with securities, loyalty programs, or real-world assets.

As such, global fintechs and crypto firms need to build a compliance infrastructure that scales with their businesses, incorporating EU crypto regulation as part of their compliance strategy.

Some firms manage compliance in-house, while others rely on outside specialists who already understand how to operationalize EU regulatory expectations within fast-moving fintech environments.

Integrating regulatory compliance into product and engineering early is no longer optional. InnReg partners with fintech innovators to help them align their business models with EU crypto rules. Click here to learn more.

Key Frameworks Under EU Crypto Regulation

EU crypto regulation is not a single law. It is a coordinated framework comprising several interlocking rules, some crypto-specific, others broader in scope but relevant.

Each regulation covers a different area: market conduct, consumer protection, AML, operational resilience, payments, and tax reporting. Together, they create a regulatory perimeter that crypto and fintech businesses can’t afford to overlook.

The sections below provide a high-level overview of the major frameworks shaping the EU crypto compliance environment as of 2026:

MiCA (Markets in Crypto-Assets Regulation)

MiCA is the foundation of EU crypto regulation. It creates a unified legal framework for crypto-asset service providers (CASPs) and token issuers across all 27 EU member states.

For fintech companies operating in or targeting the EU, MiCA is likely the first, and most important, regulation to address.

It does not cover NFTs (unless they’re fractionalized or fungible), DeFi protocols with no identifiable intermediary, or tokenized traditional financial instruments (which fall under MiFID II and other frameworks).

What MiCA Means for Crypto Businesses

MiCA introduces operational, disclosure, and risk management requirements that apply to most crypto-asset service providers (CASPs) and token issuers in the EU.

Whether a firm is launching a new product or scaling an existing one, its obligations include:

Licensing and Registration Requirements: CASPs must apply for authorization through a National Competent Authority (NCA). Approval requires a compliant business model, capital adequacy, internal governance, and clear AML controls.

White Paper and Disclosure Rules: Issuers must publish a MiCA-compliant white paper before offering or listing tokens. The document must disclose risks, token features, and project details. Marketing materials must match the white paper.

Governance, Risk, and Consumer Protection: Firms need documented governance structures, fit-and-proper leadership, and user protection processes. This includes transparent pricing, client asset safeguards, and a formal complaint-handling process.

Market Abuse and Insider Trading Provisions: MiCA prohibits insider trading, price manipulation, and false market signals. CASPs must monitor for abuse and report suspicious activity, following similar standards to those in traditional financial markets.

Stablecoin Rules and Reserve Requirements: Issuers of stablecoins (ARTs and EMTs) must maintain full reserves, offer redemption rights, and meet liquidity and reporting obligations. Larger tokens are subject to additional supervision by the European Banking Authority (EBA).

MiCA introduces new regulatory thresholds that fintech teams must account for from the outset. For fintech teams, this means evaluating product structure early. A crypto-powered feature, such as embedded custody or token issuance, could trigger licensing requirements.

As such, involving regulatory experts early helps identify potential roadblocks before they affect timelines or resources.

The EU Crypto Travel Rule (Transfer of Funds Regulation)

The EU Crypto Travel Rule extends traditional anti-money laundering (AML) requirements to crypto transfers. Under the revised Transfer of Funds Regulation (TFR), crypto-asset service providers (CASPs) must collect and transmit identifying information for both the sender and the recipient of any crypto transaction, regardless of amount.

Since the rule took effect on December 30, 2024, any business facilitating crypto transfers, whether directly or through white-label arrangements, must assess its current infrastructure to meet regulatory obligations.

Key compliance requirements of TFR include:

Data Requirements for Crypto Transfers: CASPs must collect and transmit key identifying information for both parties in any crypto transaction. Required fields include the originator’s name, wallet address, and ID number, as well as the beneficiary’s name and their wallet address.

Dealing with Unhosted Wallets: Transfers involving unhosted wallets are allowed. However, for amounts exceeding €1,000, CASPs must verify ownership of the wallet, typically through authentication methods such as message signing.

Implementation Timeline and Compliance Tools: The rule is in effect, and CASPs are expected to meet real-time data-sharing obligations immediately. Many use Travel Rule vendors or integrated compliance solutions to handle transmission, recordkeeping, and wallet screening.

For fintechs and crypto firms with fast-moving development cycles, it’s essential to assess early how transactional features map to Travel Rule triggers. Building compliance into architecture from the start is often more efficient than retrofitting controls later under regulatory pressure.

AMLD5 and AMLD6

Before MiCA and the Travel Rule, crypto businesses in the EU were already subject to anti-money laundering obligations under AMLD5 and AMLD6. These directives drew certain crypto activities into the regulatory perimeter, and they remain in effect.

AMLD5, effective since 2020, was the EU’s first step in regulating crypto. It required two categories of crypto businesses to register with national authorities and implement full AML programs:

Fiat-to-crypto exchanges

Custodial wallet providers

These firms must conduct customer due diligence (CDD), monitor transactions, and report suspicious activity, similar to traditional financial institutions.

AMLD6 expanded enforcement by:

Defining a harmonized list of predicate offenses

Extending criminal liability to senior management

Increasing penalties for non-compliance

It also improved cooperation across EU jurisdictions, making cross-border investigations easier.

If you are operating a regulated crypto business under AMLD5, you're already expected to have:

A KYC process with risk-based tiers

Internal AML policies and training

A designated MLRO (money laundering reporting officer)

Reporting capabilities for STRs/SARs

Note that MiCA and the updated Travel Rule are built on this foundation. They do not replace AMLD obligations but add to them.

Learn how Regly’s FinCrime platform helps fintech with AML screening and KYC/KYB procedures →

DORA (Digital Operational Resilience Act)

The Digital Operational Resilience Act (DORA) is the EU’s framework for managing IT and cybersecurity risks across the financial sector. As of January 2025, it applies to crypto firms licensed under MiCA.

DORA mandates that regulated entities:

Identify and assess ICT risks

Implement business continuity and disaster recovery strategies

Test systems regularly, including penetration and scenario testing

Monitor third-party service providers, especially cloud and data vendors

DORA also introduces obligations around incident reporting. Major IT incidents must be reported to regulators promptly, along with the root cause and remediation plans.

Compliance with DORA requires structured documentation, internal controls, and repeatable testing, as ad hoc processes do not meet the standard.

As such, fintech firms should treat DORA as a core component of their compliance function. Some outsource this work to compliance teams with experience in both crypto infrastructure and EU regulatory frameworks.

See also:

E-Money and Payment Rules

MiCA simplifies crypto regulation, but it does not replace e-money or payments law. If a product falls into either category, a firm must assess whether dual licensing or structural changes are required.

Under MiCA, fiat-referenced stablecoins are categorized as E-Money Tokens (EMTs). If a token is pegged 1:1 to a currency, such as the euro, it may need to be licensed not only under MiCA but also as an Electronic Money Institution (EMI).

Dual licensing is required when:

Users can redeem tokens at face value

The token is used broadly for payments

The project functions like a stored-value system

Furthermore, if a platform facilitates payment initiation, fund transfers, or account access, PSD2 might also apply.

Examples include:

Platforms enabling crypto-to-fiat payouts

Wallets with fiat on-ramps or off-ramps

Services that move user funds between accounts

In these cases, the underlying rails and user experience may resemble those of regulated payment services, triggering PSD2 obligations, such as strong customer authentication (SCA), conduct rules, and reporting requirements.

Designing around dual licensing or payments triggers? Learn more about tokenized securities →

Need help with blockchain compliance?

Fill out the form below and our experts will get back to you.

Taxation and Reporting (CARF and Beyond)

Tax compliance is not technically part of MiCA, but it’s closely adjacent and increasingly complex to separate from regulatory planning. As crypto matures, tax transparency is becoming a core expectation across the EU.

The Crypto-Asset Reporting Framework (CARF) is an OECD initiative adopted by the EU in 2023. It requires crypto-asset service providers (CASPs) to report user holdings and transactions to national tax authorities, similar to how banks report under the Common Reporting Standard (CRS).

CARF is designed to encompass:

Capital gains from crypto trading

Income from staking, lending, or token rewards

Cross-border transfers and undeclared holdings

The framework applies to individuals and entities and is designed to prevent tax evasion through the use of offshore wallets or platforms.

CASPs operating in the EU, or serving EU customers, need to:

Collect tax-relevant user data

Report trades, transfers, and crypto-based income

Identify customer residency and legal status

This introduces new compliance layers, including customer classification, transaction labeling, and coordination with national authorities. Technical implementation will likely be standardized across member states, but timelines and formats may vary.

Who Regulates Crypto in the EU?

Crypto regulation is a multi-layered system that combines national oversight with EU-level supervision. Understanding the regulatory landscape is essential for fintech and crypto companies to avoid gaps in licensing, compliance, and reporting.

The most important regulatory bodies include:

National Competent Authorities (NCAs)

Each EU member state has a financial regulator, its National Competent Authority (NCAs), that is responsible for licensing and supervising crypto firms under MiCA.

Examples of NCAs include BaFin in Germany, AMF in France, CNMV in Spain, and CONSOB in Italy.

Applicants must submit their MiCA license application to the relevant NCA in their chosen Member State. Once authorized, the NCA serves as the primary supervisory authority, overseeing ongoing obligations, including audits, regulatory disclosures, and incident reporting.

ESMA, EBA, ECB, and AMLA

At the EU level, several authorities play distinct roles:

ESMA (European Securities and Markets Authority): Develops technical standards, coordinates supervision across NCAs, and maintains public registers (including blacklists of non-compliant firms).

EBA (European Banking Authority): Focuses on stablecoin issuers and prudential standards. Oversees asset reserves, liquidity frameworks, and governance of “significant” tokens.

ECB (European Central Bank): Monitors financial stability. Can intervene if stablecoins pose a threat to monetary policy or payment systems.

AMLA (Anti-Money Laundering Authority): Launching in 2026, AMLA will directly supervise the largest cross-border crypto firms for AML/CFT compliance.

Although firms primarily interact with their designated NCA, they should anticipate involvement from EU-level authorities, particularly during the licensing process or when operating across multiple Member States.

Financial Intelligence Units (FIUs)

Financial Intelligence Units (FIUs) are national agencies responsible for receiving and analyzing reports of suspicious financial activity. Under AMLD5 and AMLD6, crypto-asset service providers (CASPs) registered or licensed in the EU are required to report such activity directly to the FIU in their home jurisdiction.

Each EU member state operates its own FIU. While the specific structure may vary, their role is consistent: to support anti-money laundering and counter-terrorist financing enforcement by identifying potential financial crime.

Crypto firms authorized under MiCA are expected to integrate this reporting into their broader AML programs. The relationship with FIUs is continuous, and reporting obligations apply not just at onboarding or during large transactions, but throughout the entire customer lifecycle.

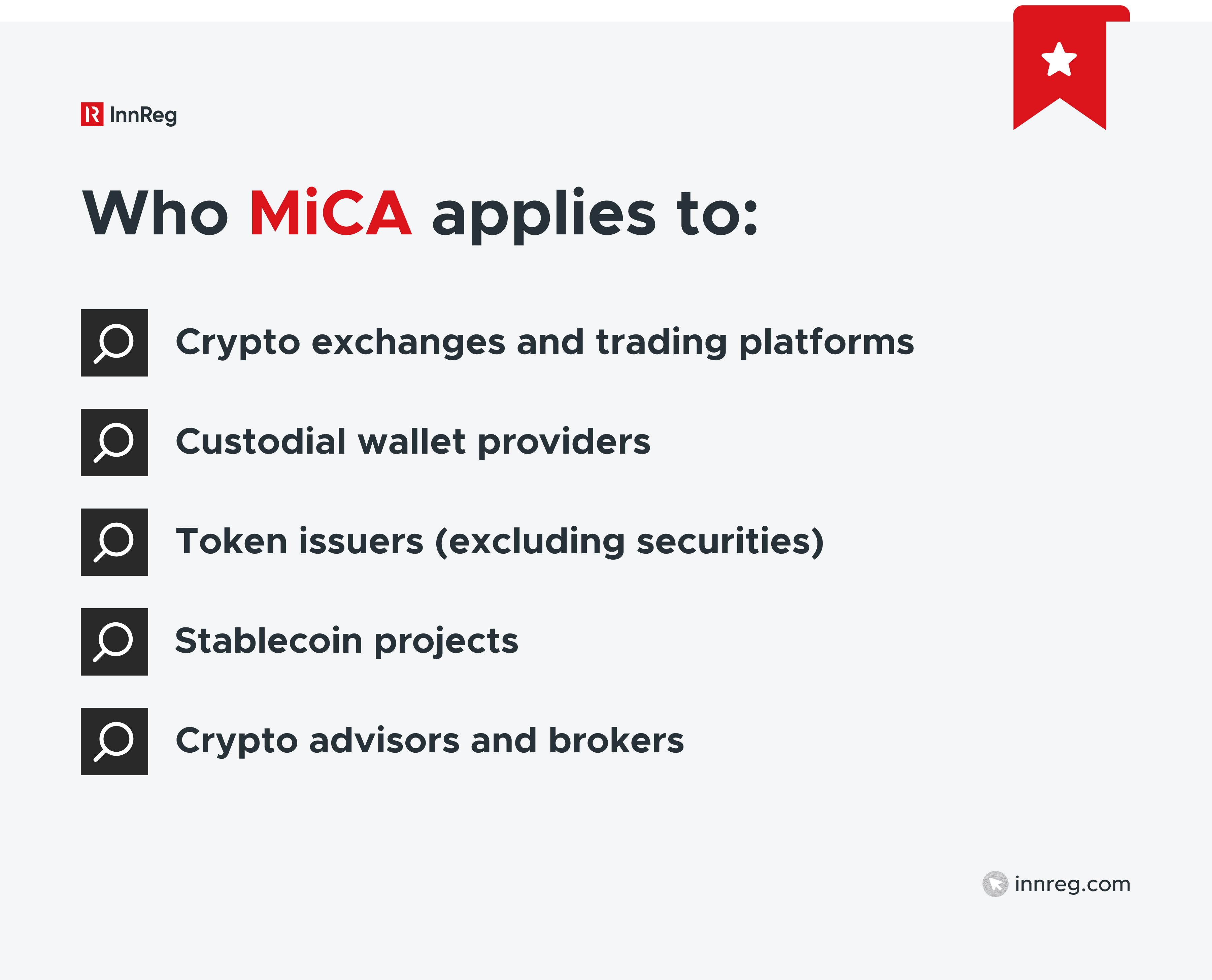

Which Businesses Fall Under EU Crypto Regulation?

EU crypto regulation is activity-based, not company-type-based. That means whether a firm qualifies as a “crypto business” depends on what it does, not how it labels itself. Many fintech companies may fall under MiCA and related frameworks, even if crypto is not their core offering.

Regulated activities include custody, trading, issuance, and exchange of crypto-assets, as well as advisory and execution services. If a business provides one or more of these services in the EU, it is likely within scope. Non-EU firms targeting EU users also fall within the scope of MiCA, regardless of their headquarters.

The most common affected business types include:

Crypto Exchanges, Custodians, Wallet Providers

These are the most obvious in-scope businesses under MiCA. Centralized exchanges must register as CASPs and comply with rules on licensing, transparency, and market conduct.

Custodial wallet providers, those holding private keys on behalf of users, also fall under the same obligations.

Both categories are subject to AMLD5, the EU Travel Rule, and MiCA’s requirements around client asset protection, operational resilience, and disclosure. Most will need to maintain internal controls comparable to those of traditional financial institutions.

Token Issuers, Stablecoin Projects, and NFT Platforms

Anyone issuing crypto-assets or tokens to the public in the EU must prepare and publish a white paper in line with MiCA.

Stablecoin issuers face additional scrutiny, including reserve management, redemption rights, and liquidity thresholds.

NFT platforms are generally excluded unless the NFTs are fractionalized or structured in a way that resembles financial instruments. If that’s the case, the issuer may fall under MiCA or even securities law, depending on the specifics.

DeFi Protocols and Cross-Border Players

Fully decentralized protocols with no identifiable operator are currently outside the scope of MiCA. However, most projects are not fully decentralized in practice. If a company builds, maintains, or markets a DeFi interface, that activity may bring it within regulatory reach.

For firms operating from outside the EU, engaging EU users triggers cross-border compliance obligations, as MiCA has an extraterritorial effect.

Marketing crypto services in the EU or onboarding EU users without local registration could lead to enforcement.

See also:

Who’s Exempt (for now)

As of 2026, certain actors and activities fall outside MiCA, including:

Central banks and public institutions

NFTs (when truly unique, non-fungible, and not part of a large series)

Crypto-assets that qualify as financial instruments under MiFID II

Protocols without a central operator or control structure

However, it is essential to note that exemptions are narrowly defined, and the list may be subject to change over time.

Regulators are already exploring future rules for DeFi, NFTs, and algorithmic stablecoins. As such, businesses in these evolving segments should monitor policy shifts and prepare for possible new obligations.

Understanding the regulatory perimeter early is critical. Some models clearly require licensing. Others sit in gray areas. In both cases, compliance obligations may arise well before launch, particularly for firms onboarding EU users, marketing within the EU, or developing infrastructure linked to crypto transactions.

Timeline: EU Crypto Regulation in Effect (2024–2026)

EU crypto regulation is already active, but not all parts take effect at once.

These are the EU crypto regulation key milestones:

MiCA: Titles III and IV (covering stablecoins) took effect on June 30, 2024. The remainder of MiCA, governing CASP licensing, disclosures, and conduct, came into force on December 30, 2024.

Transfer of Funds Regulation (Travel Rule): The Travel Rule became enforceable on December 30, 2024, with no transitional grace period.

DORA (Digital Operational Resilience Act): Applies from January 17, 2025, to all financial entities regulated under EU law, including crypto firms licensed under MiCA.

CARF (Crypto-Asset Reporting Framework): Implementation timelines vary by Member State, but most are targeting adoption by 2026, following EU-level ratification in 2023.

While the Travel Rule has no grace period, MiCA allowed transitional arrangements at the national level. Some Member States have published specific paths for temporary authorization. Others expect full compliance from the outset.

Operating without proper authorization past these deadlines can lead to enforcement, including fines, shutdown orders, and blacklisting across the EU.

Crypto and fintech businesses should treat these timelines as hard cutoffs for internal planning, given the risk of regulatory action beyond them. In practice, that means submitting licensing applications early, building internal compliance functions, and integrating controls with product and engineering roadmaps well in advance.

Common Compliance Challenges for Crypto Startups

With EU crypto rules in force, firms must adopt a forward-looking approach to regulatory planning, rather than relying on reactive adaptations.

These are the most frequent challenges businesses face:

Licensing Complexity: Firms must determine how their business model aligns with one or more regulated activities. This requires legal analysis, internal documentation, and coordination with the relevant National Competent Authority. Operating in multiple Member States adds another layer of complexity.

AML/KYC Program Gaps: Many early-stage crypto firms underestimate the operational burden of AML compliance. Basic onboarding tools fall short of EU expectations. Regulated entities must implement risk-based due diligence, transaction monitoring, and a straightforward escalation process for identifying and addressing suspicious activity. Without these elements, approval may be delayed or denied outright.

Product-Market Fit vs. Regulatory Fit: Some features that drive growth (e.g., embedded wallets, token issuance, or payment-like functionality) also trigger regulatory scrutiny. Businesses often discover too late that product architecture requires licensing, reporting, or dual oversight. Identifying these dependencies early helps avoid costly redesigns or market restrictions.

Tech Debt and Compliance Infrastructure: Manual processes and isolated tools rarely scale. Regulators expect auditable systems with documented roles, access controls, and regular testing. Retrofitting compliance infrastructure after launch is often more disruptive and expensive than building it into operations from the start.

As EU crypto regulations mature, firms that treat regulatory planning as a parallel track to product development are better positioned to scale, secure partnerships, and withstand scrutiny.

Misconceptions Founders Have About EU Crypto Regulation

Despite the growing clarity surrounding EU crypto regulation, some common misconceptions persist. These assumptions can lead to misaligned strategies, delayed approvals, or unintentional violations.

“We’re not in the EU, so it doesn’t apply.”

MiCA and other EU crypto frameworks apply based on activity, not location. If a firm targets EU users, whether through marketing, onboarding, or product access, it is likely subject to EU jurisdiction. Geofencing and disclaimers are often insufficient if the business model involves cross-border interactions.

“DeFi and NFTs are out of scope.”

True decentralization may fall outside the scope of MiCA for now, but most DeFi projects involve identifiable intermediaries, such as teams managing interfaces, liquidity, or upgrades. Similarly, NFT projects can trigger regulation if assets are fractionalized, bundled, or resemble financial instruments. Relying on current exclusions without legal review is risky.

“We’ll get compliant later.”

Waiting until launch or scale to address regulation is a common but costly mistake. Licensing timelines, technical integration, and internal controls often take months to implement. By the time the need becomes urgent, retrofitting compliance may already be delaying partnerships, banking access, or user onboarding.

Other false assumptions:

Founders sometimes believe that white-label platforms shift responsibility to vendors, that small user bases exempt them from scrutiny, or that early-stage status grants flexibility. None of these assumptions hold under current EU rules. Regulatory exposure exists from the moment a product is accessible to EU users.

Looking Ahead: What’s Next for EU Crypto Regulation?

EU crypto regulation will not remain static. Policymakers have already signaled future expansions to address emerging technologies and close perceived gaps in the current regulatory perimeter.

The following areas are already under discussion and may shape the next phase of EU crypto regulation:

Regulation of DeFi, NFTs, and AI-Driven Platforms: DeFi activity with identifiable developers, user interfaces, or governance mechanisms may eventually fall under bespoke rules or modified MiCA provisions. NFT platforms that fractionalize assets or offer financial returns may also face classification as financial instruments. The growing use of AI in trading, lending, and compliance functions could prompt new supervisory expectations, particularly around transparency and model risk.

Possible Changes in MiCA Scope: European regulators are actively assessing whether these areas warrant additional oversight. Projects with ambiguous or hybrid models may soon be subject to review.

Role of the Digital Euro: The European Central Bank’s Digital Euro initiative is likely to impact the regulation of private-sector stablecoins and wallets. If adopted, it could introduce additional technical and operational requirements for any fintech interacting with the central bank's digital currency infrastructure. That includes payment routing, settlement, identity verification, and fraud monitoring protocols.

—

As EU crypto regulations continue to evolve, firms must treat compliance as an integrated function, rather than an afterthought. That means embedding regulatory thinking into product development, engineering, and go-to-market strategies from the outset. Delays in compliance can have real consequences, including disruptions to operations, market credibility, or financing.

Whether refining a business model, entering the EU market, or reworking product architecture, involving regulatory experts early is a practical advantage. Staying ahead of EU crypto regulation is not just about meeting the rules; it is about building a business that can grow within them.

Frequently Asked Questions

What is the new crypto regulation in EU?

MiCA, Markets in Crypto-Assets Regulation, is what the EU rolled out for crypto in 2025. It creates licensing requirements for crypto service providers operating anywhere in the bloc. Exchanges, custodians, wallet services, and token issuers are all in scope.

Token launches need whitepapers now. Stablecoin operators face capital requirements. Platforms with EU customers need licenses. Once you're licensed in one member state, you can typically offer services across the others. The EU has basically decided to regulate crypto the same way it regulates traditional financial services.

Who regulates crypto in the EU?

Each EU country has its own financial regulator handling crypto oversight. The same agencies that watch over banks and payment companies. They license crypto firms and supervise what happens in their jurisdiction.

At the EU level, ESMA coordinates how MiCA gets implemented across member states. Your home country regulator is who you deal with mainly, but the EU-wide rules still apply everywhere you operate. AML enforcement runs through national financial intelligence units, with coordination happening at the EU level too.

What is a crypto regulation?

Crypto regulation is the set of rules that determines how cryptocurrency platforms and service providers can operate. It covers licensing, consumer protections, AML requirements, and disclosure obligations. The goal is to put crypto under the same kind of oversight that traditional financial services deal with.

How it works depends on where you are. Some countries require exchanges to get money transmitter licenses.

The EU created MiCA as its own crypto framework. Most regulations end up addressing similar issues, though: how you hold customer assets, monitor transactions, verify identities, and advertise your services. Even when there's no specific crypto law on the books, regulators often find ways to apply existing financial rules to crypto operations.

Ani is a Senior Compliance Consultant with over 10 years of experience in legal and regulatory compliance across fintech, RegTech, and cross-border payments. She has held roles at Remote and EY, with expertise in AML, GDPR, financial crime, and EU regulatory frameworks. She holds CAMS and CIPP/E certifications.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with blockchain compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts