FINRA Continuing Membership Application (CMA) Guide

The FINRA Continuing Membership Application (CMA) is a crucial step for broker-dealers and other regulated firms when making significant changes to their business operations.

Whether it is a merger, a shift in ownership, or the launch of a new business line, the CMA process determines whether FINRA will allow the firm to move forward.

For fintech companies, where innovation often pushes against traditional boundaries, knowing how the CMA works can make the difference between timely approval and costly delays.

This guide explains when a CMA is required, outlines the process, and describes how FINRA evaluates applications.

At InnReg, we help broker-dealers, ATSs, and crowdfunding portals manage FINRA Continuing Membership Applications (CMAs), from materiality assessments and CMA strategy to documentation, projections, and interactions with FINRA’s MAP team. Contact us to learn more.

What Is a FINRA CMA?

A FINRA Continuing Membership Application (CMA) is the filing a broker-dealer must submit when planning a significant change in ownership, control, or operations. The application allows FINRA to review whether the firm will continue meeting its regulatory obligations under the new structure. What you need to know when buying a broker-dealer →

Unlike the New Membership Application (NMA), which is required when a firm first seeks FINRA membership, the CMA applies to existing members making material changes to their ownership, structure, or operations. In practice, the CMA serves as a checkpoint: before expanding into new business lines or altering its corporate structure, a firm must demonstrate that it has the necessary financial, supervisory, and compliance capacity to manage the change.

For broker-dealers, the CMA is a core part of maintaining good standing with FINRA. Changes such as mergers, new lines of business, or onboarding new principals are routine in the industry, but they all raise supervisory and investor protection considerations. The CMA review is where FINRA evaluates those risks.

Read our broker-dealer registration guide →

Fintech firms tend to adjust their business models more often than traditional businesses and experiment with areas such as digital assets, fractional shares, or mobile-first platforms. These developments introduce risks that do not always align precisely with traditional regulatory frameworks.

When filing a CMA, the firm must frame its new initiatives in regulatory terms, providing business plans, financial projections, supervisory procedures, and demonstrating the qualifications of key staff. Compliance consulting firms like InnReg can help broker-dealers navigate regulatory challenges related to CMA filing.

When a FINRA CMA Is Required

Not all business changes trigger a CMA. It applies only when certain events alter the ownership, structure, or scope of a broker-dealer’s activities in ways that FINRA considers material.

The most common triggers include:

Ownership or Control Changes: A CMA is required when a change in ownership results in an individual or entity owning or controlling 25% or more of the broker-dealer. This can happen through the sale of shares, new investment, or partner buyouts. Even internal ownership transfers can cross the threshold.

Mergers, Acquisitions, and Asset Transfers: If a firm merges with another broker-dealer, acquires a member firm, or transfers 25% or more of its assets or earnings, a CMA is needed. FINRA reviews whether the combined business will have the capital, systems, and supervisory structure to comply with securities rules..

Material Changes in Business Operations: A CMA is often required when a broker-dealer expands into a new line of business, adds services that demand higher net capital, or significantly increases the scale of its activities. For example, moving from introducing broker status to carrying broker status represents a material shift in both operational and financial responsibilities.

Membership Agreement Restrictions: Many firms have restrictions built into their FINRA membership agreement at approval. If you want to remove or modify a restriction, such as caps on the number of reps or limits on business activities, you generally must file a CMA.

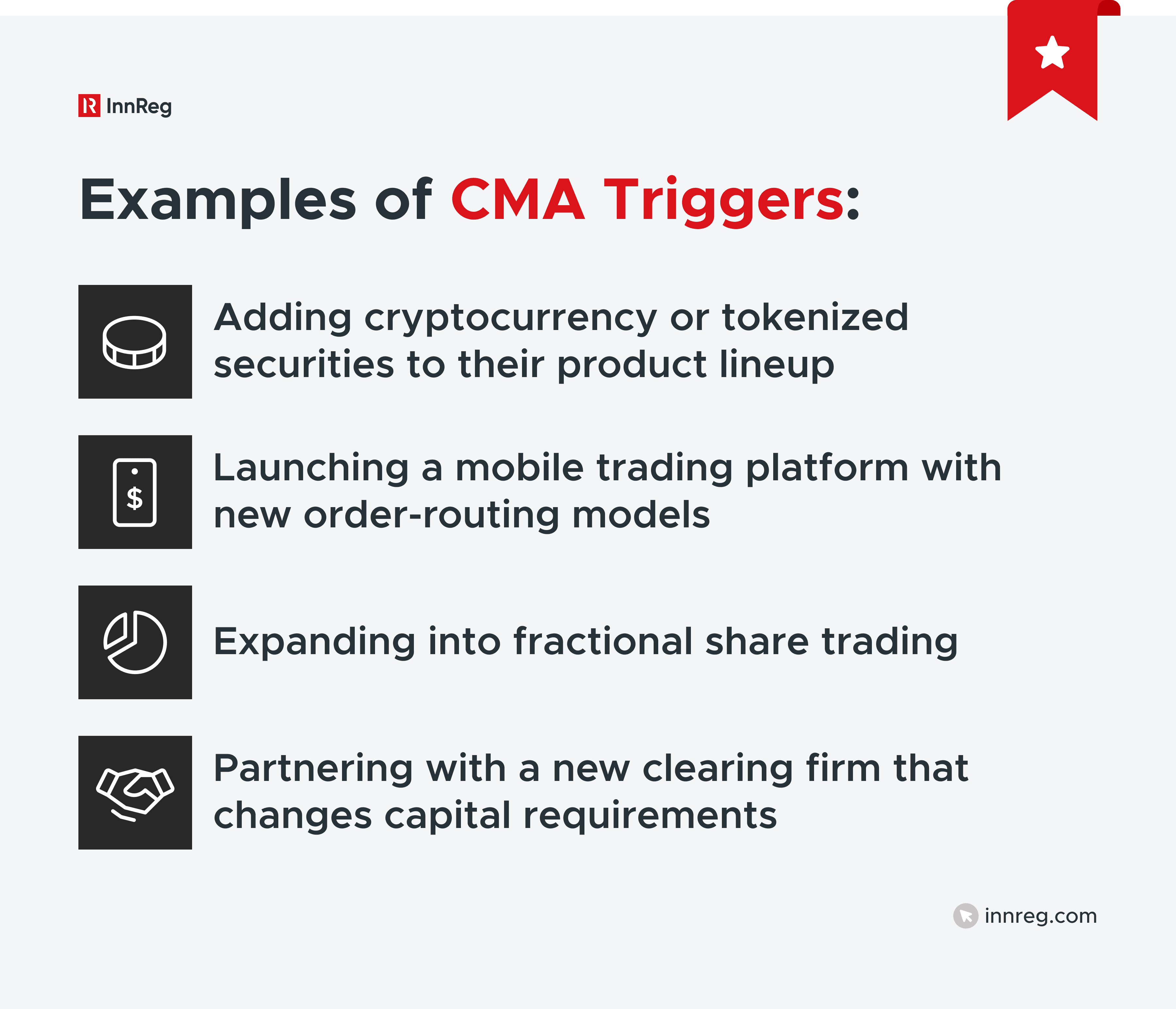

Fintech broker-dealers often encounter CMA requirements when they expand into innovative products or adopt new operating models. Adding cryptocurrency or tokenized securities to their platform, for instance, introduces unique custody and trading challenges that FINRA reviews as material changes. The same applies when a firm launches a mobile-first trading system that alters order routing or customer interaction.

The Safe Harbor for Business Expansions

FINRA provides a safe harbor framework that allows firms to grow modestly without triggering a formal application, as long as certain conditions are met, meaning that not every business expansion needs a CMA.

To qualify, the firm must have a clean compliance record and no restrictions in its membership agreement related to expansion. Within that framework, a broker-dealer can add a limited number of new representatives, open a small number of additional offices, or expand its market-making activity within set thresholds.

However, expansions that go beyond these limits, or firms with recent disciplinary issues, fall outside of the safe harbor. In those cases, FINRA expects the member to consult with its assigned analyst or file a CMA before making changes.

For fintech firms, where growth can happen quickly, this distinction is critical. Adding ten new sales reps over a year may not require a CMA, but launching a new platform or expanding into digital assets almost certainly will.

Learn more about FINRA rules →

CMA vs. Other Filings

Not all regulatory filings carry the same weight or purpose as a FINRA CMA. One of the most common sources of confusion for founders and compliance officers is knowing when a CMA is required versus when a different filing is sufficient.

CMA vs. NMA

The New Membership Application (NMA) is the filing a firm must submit when it seeks to become a FINRA member for the first time.

It is a comprehensive review where FINRA evaluates the applicant’s business plan, financial resources, supervisory procedures, and the qualifications of key personnel before granting membership. In short, the NMA is about entry into the industry. Unlike CMAs, where FINRA may request a membership interview at its discretion, NMAs require the Department to conduct a membership interview before issuing a decision under Rule 1013.

By contrast, the Continuing Membership Application (CMA) applies only to existing FINRA members. Instead of assessing whether a firm is ready to operate, the CMA evaluates whether an established broker-dealer can continue to meet regulatory obligations while undergoing a significant change. These changes may involve new ownership, a merger, or a shift into additional business lines.

CMA vs. Form BD Amendments

Form BD is the foundational registration document for broker-dealers. Firms update it to reflect changes such as new addresses, business activities, or ownership information.

However, submitting an amendment to Form BD is not the same as filing a CMA. FINRA explicitly requires a CMA for material changes, even if the information is already reported through Form BD.

Learn more about Form BD →

CMA vs. Membership Agreement Change (MAC) Requests

In certain situations, a firm may not need a full CMA but still has to update its membership agreement. FINRA allows for a MAC request when the change is non-material (for example, dropping an unused line of business or reducing net capital requirements). A MAC request is simpler, carries no filing fee, and is handled through FINRA Gateway.

See also:

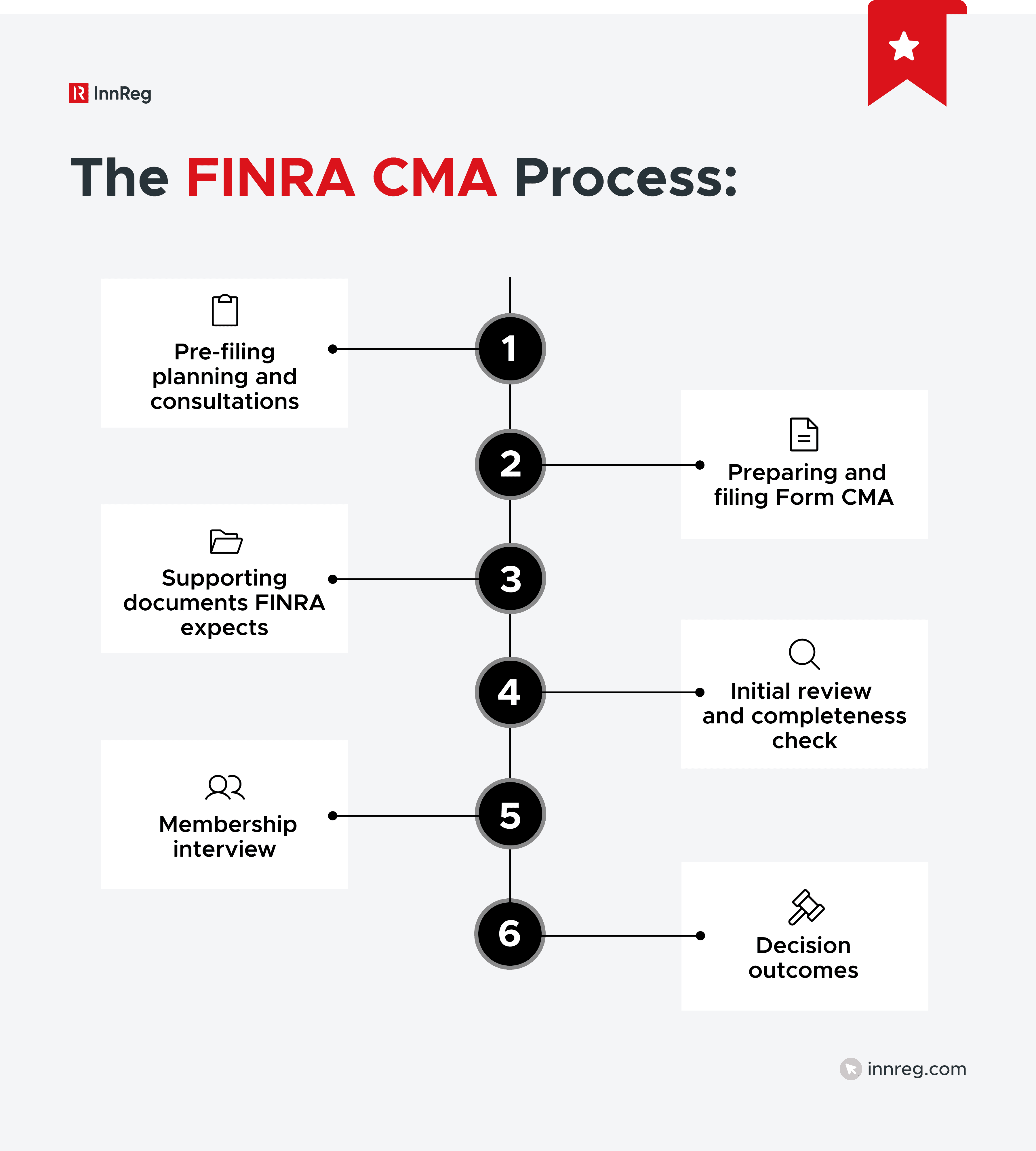

The FINRA CMA Process Step-by-Step

Reviewing a FINRA CMA involves multiple stages, each with its own documentation and review cycle. Understanding this sequence helps firms prepare and avoid unnecessary slowdowns.

Need help with broker-dealer compliance?

Fill out the form below and our experts will get back to you.

1. Pre-Filing Planning and Consultations

Before filing a CMA, many firms consult with compliance experts to assess whether the planned change is material and to determine the necessary documentation.

For fintech firms, where business models often raise novel regulatory questions, working with experienced advisors like InnReg can help clarify expectations and avoid unnecessary delays in the process.

2. Preparing and Filing Form CMA

The application is submitted through FINRA Gateway using the Form CMA template. Firms must provide details about the change, business plan updates, ownership structure, financial projections, and supervisory procedures. Supporting evidence (transaction agreements or vendor contracts, etc.) can mitigate regulatory risks related to the filing.

Submitting a CMA also requires payment of a FINRA application fee. These fees are tiered based on the size of the member firm, with larger firms paying higher amounts. While the fee is not the primary hurdle in the process, it is an upfront cost that should be factored into planning timelines and budgets.

3. Supporting Documents FINRA Expects

Alongside the form, firms typically include pro forma financials, organizational charts, capital source documents, and revised compliance procedures. FINRA places particular weight on whether supervisory staff hold the required licenses for the expanded business.

4. Initial Review and Completeness Check

Once filed, the CMA enters an intake review. FINRA staff assess whether the submission is “substantially complete.” If important information is missing, the application is delayed or rejected. Timely and thorough responses at this stage make the process more efficient.

5. Membership Interview

Under FINRA Rule 1017, the Department may require the applicant to participate in a membership interview as part of the CMA review. While not mandatory in every case, interviews are common in practice, particularly when the proposed change involves new business lines, complex ownership structures, or innovative models.

If an interview is requested, FINRA will typically meet with firm leadership and key principals. The discussion focuses on management’s understanding of the proposed changes, supervisory structure, financial projections, and compliance controls. For fintech firms, this is often where regulators probe how new technology or products will be supervised in practice.

6. Decision Outcomes

At the end of the process, FINRA issues one of three outcomes: approval, approval with conditions, or denial. Conditional approvals may limit activity or impose reporting obligations. Denials are rare but can happen if a firm cannot demonstrate financial or supervisory readiness.

See also:

Key Regulatory Considerations

Understanding the regulatory framework behind a FINRA CMA is essential for firms planning changes.

The rules go beyond FINRA, and filings often interact with broader SEC and state requirements:

FINRA Rule 1011 and 1017 Triggers

The main rule is FINRA Rule 1017, but FINRA Rule 1011 and its associated Interpretive Materials also help guide when a CMA must be filed.

This rule covers ownership and control changes, mergers, asset transfers, and material business expansions.

If the change affects the firm’s scope of activity or governance in a meaningful way, it likely falls under Rule 1017.

Learn about 9 key FINRA rules affecting fintechs →

SEC Net Capital Requirements

Many CMA filings touch on SEC Rule 15c3-1, the net capital rule. For example, moving into a business line that requires higher capital, such as becoming a carrying broker, demands that firms show they can meet and maintain new, higher minimum levels of capital.

FINRA will review pro forma financials, funding sources, and capital adequacy as part of the CMA package.

Interaction With Other Regulators

CMA requirements also intersect with other regulatory bodies.

A state securities regulator may need to be notified of ownership changes. The SEC may require updates to Form BD. Firms that operate internationally could face parallel requirements with regulators such as the FCA in the UK or ESMA in the EU.

For fintech firms with cross-border operations, coordinating these obligations can be as important as the FINRA filing itself.

InnReg provides regulatory and product strategy services to help fintechs navigate their obligations →

Recent Updates and Enforcement Trends

The FINRA CMA process has evolved in recent years, and these updates reflect the effort to adapt to industry innovation and to address gaps.

FINRA’s MAP Program Transformation

FINRA has made structural changes to its Membership Application Program (MAP) in an effort to streamline reviews.

Applications now go through an initial “triage” stage to confirm completeness before the formal review clock starts.

Specialized teams, such as those focusing on fintech or trading, handle reviews, which helps FINRA ask more targeted questions, while guidance checklists, including those for digital assets, give firms a clearer picture of what documentation to prepare.

New Rules for High-Risk Individuals and Customer Claims

Rule 1017 was revised to capture situations where high-risk individuals seek ownership or principal roles at member firms.

If a candidate has a history of serious disciplinary issues or certain criminal events, the firm must request a materiality consultation.

Similarly, if a firm with pending arbitration claims or unpaid customer awards wants to transfer assets, FINRA requires pre-review to protect investors.

See also:

Enforcement Actions for CMA Violations

FINRA has not hesitated to sanction firms that failed to file a CMA when required. In recent years, firms have been fined for expanding branch networks beyond membership agreement limits or allowing ownership transfers without prior approval.

Penalties vary but often include monetary fines and public censure, highlighting that failing to treat CMA requirements seriously can have both financial and reputational consequences.

—

For fintechs, these trends show that new or experimental models face closer scrutiny during CMA reviews. Digital assets, mobile-first platforms, and novel clearing arrangements frequently trigger material change determinations.

While FINRA is building guidance to address innovation, firms should anticipate longer review cycles and more detailed requests when their models depart from traditional practices.

Common Challenges in the CMA Process

Even with careful planning, firms often encounter hurdles when preparing and submitting a FINRA CMA. These challenges can slow the review or, in some cases, lead to enforcement action if the filing is missed entirely.

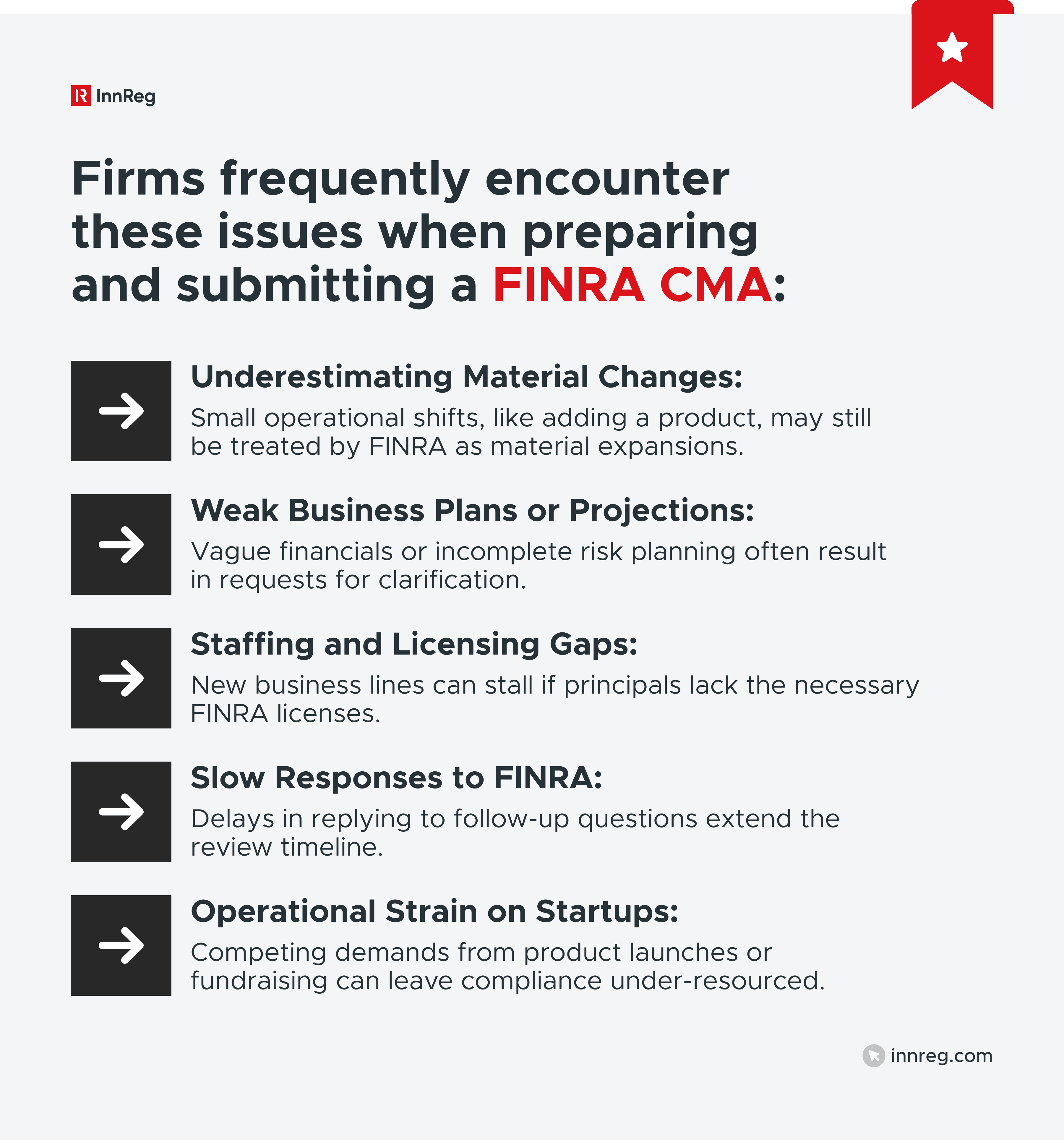

Underestimating What Counts as “Material”

One of the most frequent mistakes is assuming that a business change is too small to trigger a CMA.

For example, adding a new product or shifting order flow may feel operational, but FINRA may view it as a material expansion. Failing to confirm with FINRA before moving forward risks delays or penalties.

Incomplete Business Plans or Financial Projections

Applications that do not provide enough information in their business plans or capital forecasts are often sent back for clarification.

FINRA expects specifics: projected revenues, expenses, capital sources, and risk management procedures tied directly to the proposed change. Vague or high-level plans tend to extend the review process.

Staffing and Licensing Gaps

Another frequent issue arises when firms propose a new business line without having principals or staff in place with the required FINRA licenses.

For example, expanding into general securities supervision without a Series 24 principal will hold up the application.

Similarly, if the business plan includes an investment company and variable contracts, FINRA expects to see a qualified Series 26 supervisor on staff.

Read our guide for a breakdown of all FINRA exams and licenses →

Slow Responses to FINRA

The CMA process typically involves multiple rounds of information requests. Firms that delay responding risk pushing the timeline well beyond the 180-day review window. Keeping internal resources aligned to respond quickly is critical.

Operational Strain on Startups

For fintech startups, the CMA process often competes with product launches, fundraising, or hiring priorities. Without sufficient compliance support, applications may lag or lack the level of detail FINRA expects.

InnReg provides compliance support to broker-dealers →

Best Practices for a Successful CMA

While the FINRA CMA process can be demanding, firms that approach it strategically often move through the review more efficiently.

The following practices address the most common challenges and help set realistic expectations:

Early Engagement with FINRA: Engage FINRA’s Membership Application Program staff before filing. A pre-filing meeting or materiality consultation clarifies whether a CMA is required and what documentation FINRA will expect.

Using FINRA’s Checklists and Fintech-Specific Guidance: Incorporating FINRA’s checklist into the application process will help you align your filings with the current regulatory priorities and provide the necessary information.

Preparing Compliance Documentation in Advance: Strong CMA submissions include updated supervisory procedures, pro forma financials, and clear business plans. Preparing these in advance, rather than reacting to FINRA’s requests, keeps the review moving.

Managing Project Timelines Realistically: The CMA review can take months. Building compliance deadlines into the broader business plan prevents last-minute conflicts with product launches, capital raises, or hiring schedules.

Considering External Expertise: For startups and lean compliance teams, outsourcing parts of the process to experienced compliance consultants can reduce strain. A team that understands fintech-specific CMA requirements can provide the depth that a single in-house officer may not have.

At InnReg, we help fintechs navigate the CMA process. Contact us to learn more about our services.

—

The FINRA CMA serves as a checkpoint to determine whether a broker-dealer can expand, restructure, or adapt its business while continuing to meet FINRA’s standards.

For traditional firms, the requirements are well-established. Still, for fintech broker-dealers, the process often intersects with innovation in areas such as digital assets, mobile platforms, and new clearing models.

Filing a CMA requires fintechs to present business plans, demonstrate adequate financial resources, and show that qualified supervisory staff are in place.

InnReg was founded in 2013 by Francesco Matteini, former Chief Compliance Officer who helped launch and scale some of the most innovative digital broker-dealers over the last two decades. He built compliance programs to support the first zero-commission broker and the first BD-sponsored investor social network. Since its founding, InnReg has attracted highly experienced fintech consultants with long careers in compliance, risk management, and a deep understanding of the fintech industry.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with broker-dealer compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts