Form BD vs. Form CMA: Key Differences Explained

Mar 31, 2026

·

10 min read

If you are confused about the differences between Form BD vs. Form CMA, it usually means your firm is at a decision point. You may be registering for the first time or considering a change in how your broker-dealer operates.

Although the forms are related, they are used for different regulatory purposes. Mixing them up can create unnecessary delays and confusion, especially for fintech firms with complex or evolving models.

This article breaks down the differences between Form BD and Form CMA and explains how each one is used in practice so that you can plan filings and next steps more confidently.

At InnReg, we help broker-dealers and fintech firms navigate Form BD, Form CMA, and ongoing regulatory obligations. From registration and licensing to compliance program development and day-to-day compliance operations, our team supports firms as an outsourced compliance department or an extension of in-house teams. Contact us to learn more about InnReg’s broker-dealer compliance services.

What Is Form BD?

Form BD is the application a firm files to register as a broker-dealer in the US. It's the starting point for SEC registration and the first step toward FINRA membership.

This filing gives regulators a clear picture of the business, and covers:

Who owns and controls the firm

Activities it plans to conduct

How it will generate revenue

Any relevant regulatory history.

Each section helps regulators assess how the firm intends to operate within the broker-dealer framework.

For fintech firms, this process often goes beyond a standard description. Products built on new technology, unconventional structures, or layered partnerships can lead to additional questions during review.

How the business is described in Form BD shapes early regulatory expectations, which makes careful and accurate drafting especially important.

For a deeper walkthrough of the filing process, see Form BD: What It Is, Who Needs It, and How to File It →

What Is Form CMA?

Form CMA is the filing that existing broker-dealers use to notify FINRA of material changes. It's used when a firm wants to modify its approved activities, structure, or operations. In this case, “CMA” stands for “Continuing Membership Application.”

Rather than registering a new firm, Form CMA focuses on what has changed. This can include updates to business lines, ownership, supervisory structure, or key service providers. FINRA then reviews these changes to determine whether they raise new regulatory considerations.

For fintech firms, Form CMA often comes into play as the business evolves. New products, partnerships, or technology-driven processes can trigger a filing even when the core registration remains the same.

For a step-by-step overview, see our FINRA Continuing Membership Application (CMA) Guide →

Form BD vs. Form CMA: Quick Comparison

Although both filings are part of the broker-dealer's application for registration, they address different regulatory matters. One establishes a firm’s regulatory footprint, while the other governs how that footprint changes over time.

Here’s how both forms differ.

Aspect | Form BD | Form CMA |

|---|---|---|

Filing objective | Apply for broker-dealer registration | Request approval for material changes |

Regulator involvement | SEC and FINRA | |

Timing | Before operations begin | After initial registration |

Level of detail | Firm-wide disclosures | Change-specific disclosures |

Common use cases | New market entry | Product, structure, or control changes |

For fintech firms that evolve quickly, this distinction has real operational impact. Choosing the correct filing affects review timelines, regulatory questions, and how planned changes are evaluated. That makes early alignment especially important.

Who Needs to File Form BD or Form CMA, and When?

Whether a firm files Form BD or Form CMA depends on where it's in its regulatory lifecycle and what it plans to do next. The key factor is whether the firm is seeking initial approval or proposing a change to an existing registration.

Startup Registration Timeline: When Form BD Applies

For startups entering the broker-dealer space, Form BD comes into play early. It's filed before the firm can begin any broker-dealer activity and sets the sequence for the entire registration process.

The filing typically happens after the business model is defined but before systems, vendors, and staffing are fully in place. Regulators review Form BD alongside related documents and agreements to understand how the firm plans to operate and supervise its activities.

For fintech startups, this timing can be challenging. Product development and regulatory review often move at different speeds. Aligning Form BD disclosures with realistic operational plans helps avoid revisions and delays later in the process.

Operational Changes: When Form CMA Applies

Form CMA becomes relevant once a broker-dealer is already registered and wants to materially change how it operates. It's required when a planned update goes beyond the scope of the firm’s current approvals.

These changes can take many forms. Common examples include:

Launching a new product

Adding a new line of business

Changing ownership or control

Modifying supervisory or clearing arrangements.

Each change is reviewed in the context of the firm’s existing membership.

For fintech firms, evolution is often part of the business model. As products mature or partnerships shift, Form CMA helps regulators assess those changes before they are implemented. Planning for CMA filings early makes it easier to adjust timelines and internal resources.

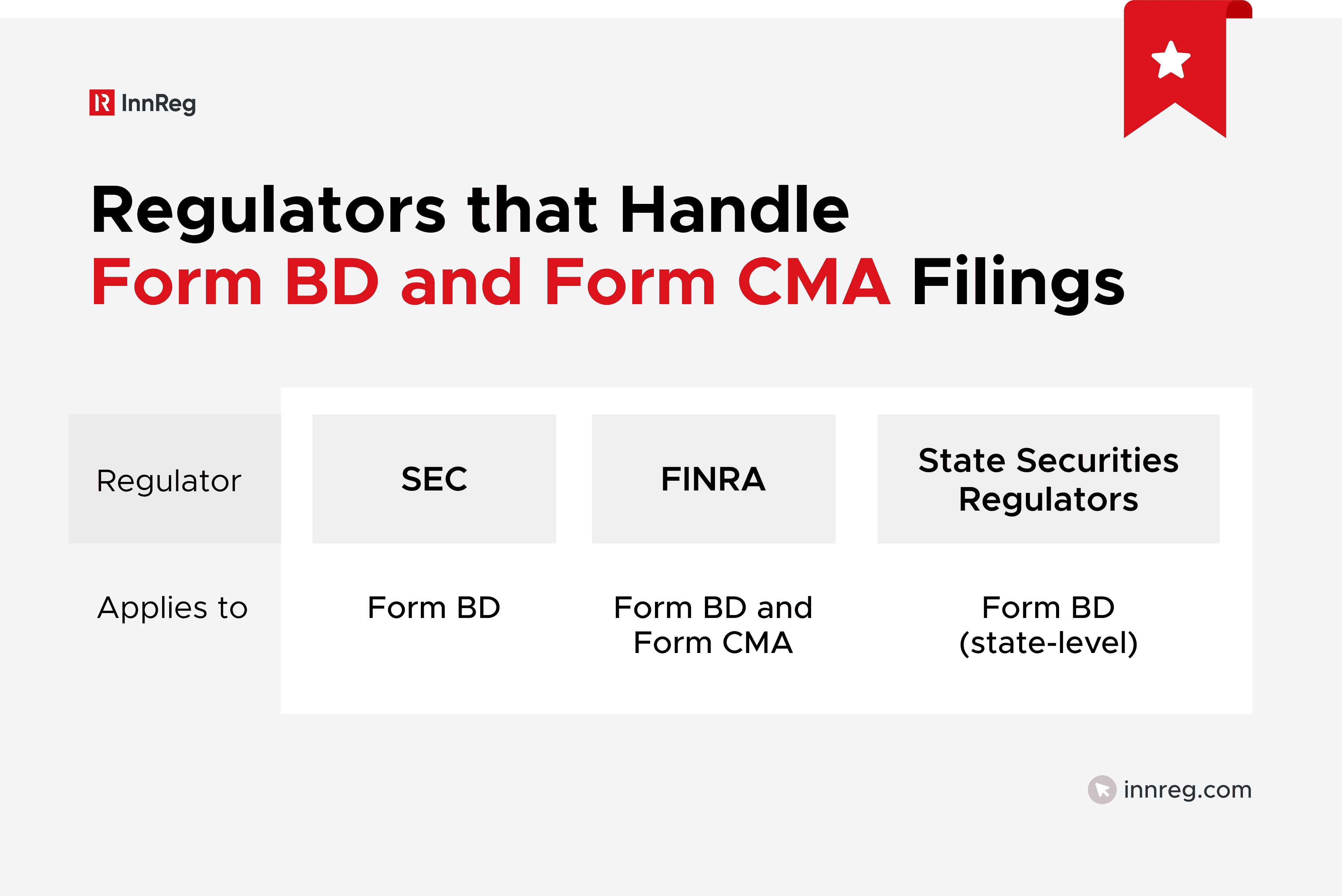

Which Regulators Handle Form BD and Form CMA Filings?

The type of filing and the stage of the firm’s lifecycle determine which regulators review Form BD and Form CMA. Knowing who is involved helps firms understand how decisions are made and what to expect during review.

See also:

SEC Oversight for Form BD

The SEC reviews Form BD as part of the broker-dealer registration process. Its role is to evaluate whether the firm’s proposed activities align with federal securities laws.

That review focuses on core disclosures, including ownership, control, business activities, and any disciplinary history. The SEC uses this information to understand how the firm plans to operate and where regulatory risk may arise.

For fintech firms, questions often come up around product structure and investor protections, especially when technology plays a central role. Clear and consistent explanations help reduce the back-and-forth during the process and keep it on track.

Need help with fintech compliance?

Fill out the form below and our experts will get back to you.

FINRA’s Role in Reviewing Form BD and Form CMA

FINRA reviews both Form BD and Form CMA, but its focus differs depending on the type of filing. For new registrations, FINRA evaluates whether the firm is prepared to meet its membership and supervisory obligations.

During a Form BD review, FINRA looks at the firm’s supervisory structure, written supervisory procedures, staffing, and vendor relationships. The goal is to understand how the firm will handle day-to-day compliance once it begins operating.

For Form CMA filings, FINRA’s review is more targeted. The firm is already a member, so FINRA focuses on how the proposed change affects existing approvals and controls. This narrower review often centers on whether current systems and supervision can support the update.

State Securities Regulators and Form BD

State securities regulators may also be involved when a firm files Form BD. This typically happens when a broker-dealer plans to operate in one or more states or maintain a physical presence there.

States review Form BD information to confirm that the firm meets local registration and notice requirements. Some states conduct a limited review, while others may ask follow-up questions based on the firm’s activities or target customer base.

For fintech firms operating across multiple states, this layer can add complexity. Understanding state-level expectations early helps firms coordinate filings and avoid gaps as they expand their footprint.

Why Form CMA Is a FINRA-Only Process

Form CMA filings are submitted by firms that are already FINRA members. That’s why they are reviewed exclusively by FINRA.

Once a broker-dealer is registered, FINRA becomes the primary regulator overseeing how the firm operates day to day. When a firm proposes a material change, FINRA evaluates whether that change fits within the existing regulatory framework and supervisory structure.

Keeping the process within FINRA helps streamline review and oversight. It also allows proposed changes to be evaluated by the regulator most familiar with the firm’s operations and compliance history.

What Triggers a CMA Filing?

Form CMA is triggered when a broker-dealer plans to make a material change that affects how it operates. The key question is whether the update is considered material under FINRA rules.

FINRA’s Safe Harbor Rules

FINRA’s safe harbor rules lay out certain situations where a broker-dealer can make changes without filing Form CMA. These are limited to changes that don’t materially affect the firm’s business, risk profile, or supervisory structure.

Some of the examples that usually fall under safe harbor include small increases in business volume, adding people to roles the firm already has, or updating technology that doesn’t change how work is supervised.

As long as the firm stays within its existing approvals, these updates can typically move forward without a Form CMA.

Safe harbor does not remove oversight altogether. Firms still need to document their analysis and keep records showing why a CMA was not required. This documentation is often reviewed during exams and should be prepared with that in mind.

Examples of Material Changes

A material change is a change that meaningfully affects how a broker-dealer operates or how regulators view its risk. These aren’t routine updates or minor tweaks. They’re the kinds of changes regulators expect to hear about ahead of time, which is why they usually require advance notice through Form CMA.

Common examples include:

Launching a new product or service

Adding an activity that increases a firm’s required capital

Adding a new line of business

Changes to ownership or control (above the de minimis threshold)

Modifying clearing, custody, or introducing broker arrangements

Updates to supervisory structure or reporting lines

Changes to compensation models tied to regulated activity

Adding or replacing key third-party vendors

For fintech firms, material changes often arise as products mature or new partnerships are introduced. When a change affects customer interaction, supervision, or revenue generation, it's often viewed as material by FINRA.

See also:

What Doesn’t Trigger a CMA Filing (But Still Requires a BD Update)?

Not every change needs a Form CMA. Some updates are more administrative or informational and can be handled with a Form BD amendment instead. These changes don’t affect the firm’s approved activities or how it’s supervised.

Common examples include:

Changes to addresses or contact details

Updates to titles where responsibilities stay the same

Replacing individuals in existing roles without altering reporting lines.

Routine ownership changes that stay below control thresholds may also fall into this category.

Even though these updates are lower impact, they still matter. Keeping Form BD current helps avoid inconsistencies during exams and prevents small gaps from becoming larger regulatory issues over time.

Timeline and Review Process After You File

After a Form CMA is filed, firms often want to know how long the review will take and what happens next. Understanding the typical timeline helps teams plan changes without unnecessary disruption.

How Long CMA Reviews Take

The length of a CMA review really depends on the type of change and how clearly it’s explained. Simpler updates typically move faster, while more complex changes usually take a bit longer and come with a few extra questions along the way.

Simple changes may wrap up in just a few weeks, while filings tied to new products, business lines, or ownership changes can take several months. Timing also depends on how quickly a firm responds to FINRA’s follow-up questions.

For fintech firms, timelines can extend when changes involve new technology or third-party providers. Building flexibility into project plans helps teams manage reviews without stalling broader business goals.

What to Expect During FINRA’s Review

During a CMA review, FINRA usually asks questions to better understand the proposed change. Those questions often focus on supervision, controls, and how the update fits into the firm’s existing structure.

Firms may be asked to share revised policies, updated procedures, or more details on workflows and vendor relationships. In some cases, FINRA asks follow-up questions to confirm the change doesn’t introduce new risks.

For fintech firms, reviews often dig into how technology supports compliance in practice. Clear documentation and timely responses help keep things moving and cut down on extra back-and-forth.

Interview, Conditions, and Approval Outcomes

In some CMA reviews, FINRA may ask for a call to talk through the proposed change. These conversations help clarify how the firm plans to supervise the update and support it in day-to-day operations.

Depending on the filing, FINRA may approve the change as submitted or approve it with conditions. Those conditions can include extra reporting, updated procedures, or limits on how the change is rolled out.

For fintech firms, this is a standard part of the process, not a setback. Knowing the possible approval paths ahead of time helps teams prepare internally and avoid last-minute scrambles.

—

Questions around Form BD vs. Form CMA usually pop up during milestones like registration, expansion, or operational changes. When teams know which filing applies, they can plan ahead and avoid unnecessary friction with regulators.

For fintech firms, these filings often come hand in hand with new products, partnerships, or technology updates. Taking a clear, realistic approach to timing helps everything move forward smoothly, without disrupting day-to-day operations.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with compliance, reach out to our regulatory experts today:

Last updated on Mar 31, 2026

Related Articles

Featured LinkedIn Posts