FinCEN Form 8300: Cash Reporting Requirements for Businesses

FinCEN Form 8300 is one of the most important reporting tools businesses need to understand when handling large cash transactions. The form creates a record that helps regulators detect money laundering, tax evasion, and other financial crimes.

This article outlines what Form 8300 covers, who must file it, what counts as “cash,” and the key requirements firms should be aware of. Along the way, we’ll break down practical steps compliance teams can follow and provide a comparison with the more familiar Currency Transaction Report (CTR).

We’ve provided clear, accurate, and actionable information so that, by the end, you’ll know when Form 8300 applies, how to file correctly, and what regulators expect.

At InnReg, we help MSBs, money transmitters, and fintech platforms build and operate AML and BSA reporting programs, including Form 8300 processes, CTR workflows, and staff training. Our team supports you in aligning cash reporting procedures with your broader compliance framework. Contact us to learn more.

What Is FinCEN Form 8300?

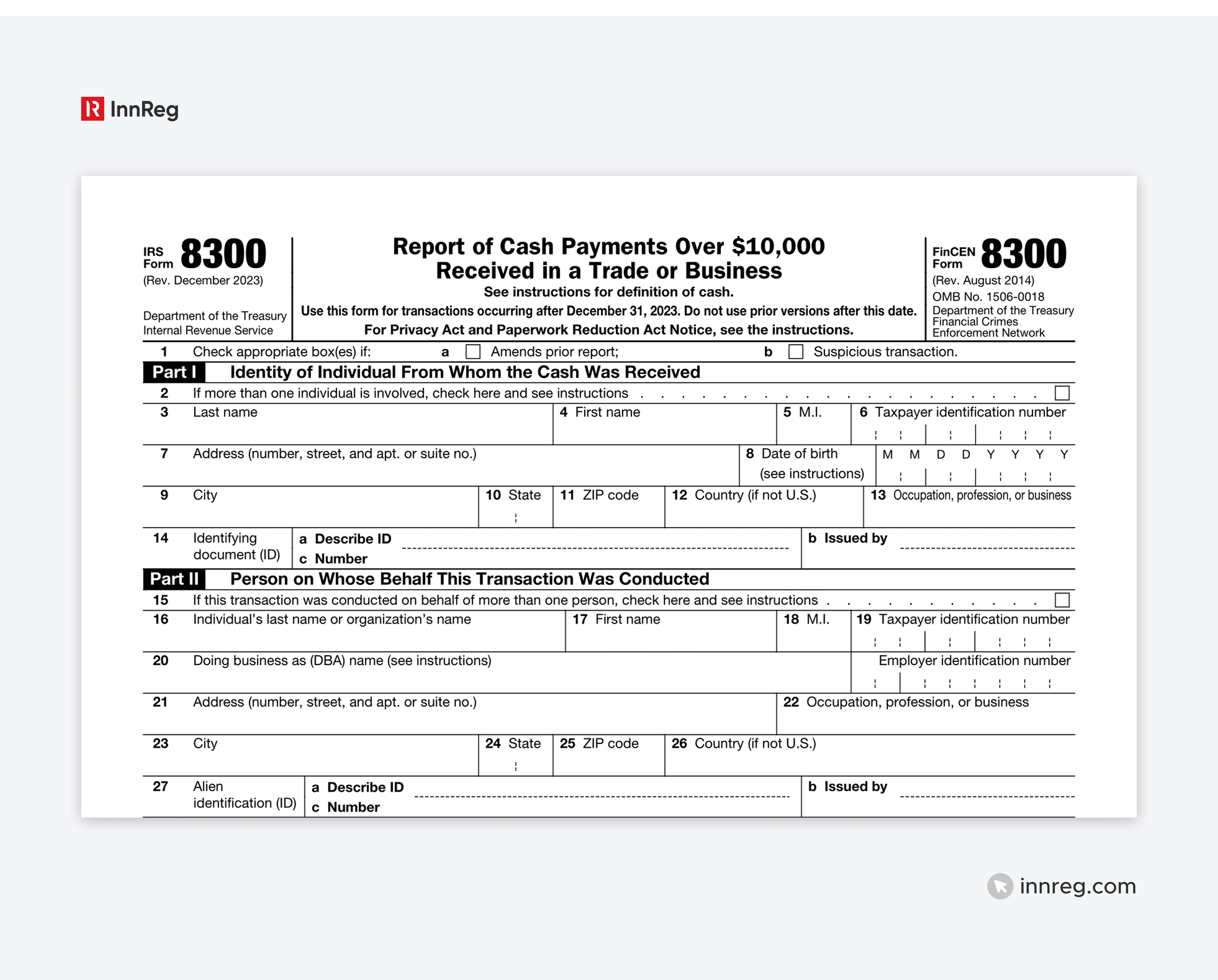

FinCEN Form 8300 is officially titled Report of Cash Payments Over $10,000 Received in a Trade or Business. It is a joint form issued by the Internal Revenue Service (IRS) and the Financial Crimes Enforcement Network (FinCEN). Businesses must file it when they receive more than $10,000 in cash from a single transaction or from related transactions.

The purpose of Form 8300 is to create an official record of large cash payments. Regulators use these filings to track unusual or suspicious financial activity that may point to money laundering, drug trafficking, or tax evasion. The information collected includes the amount, date, method of payment, and identifying details of the person making the payment.

For compliance officers, understanding when and how to file Form 8300 is a baseline requirement, even if cash transactions are rare in your jurisdiction.

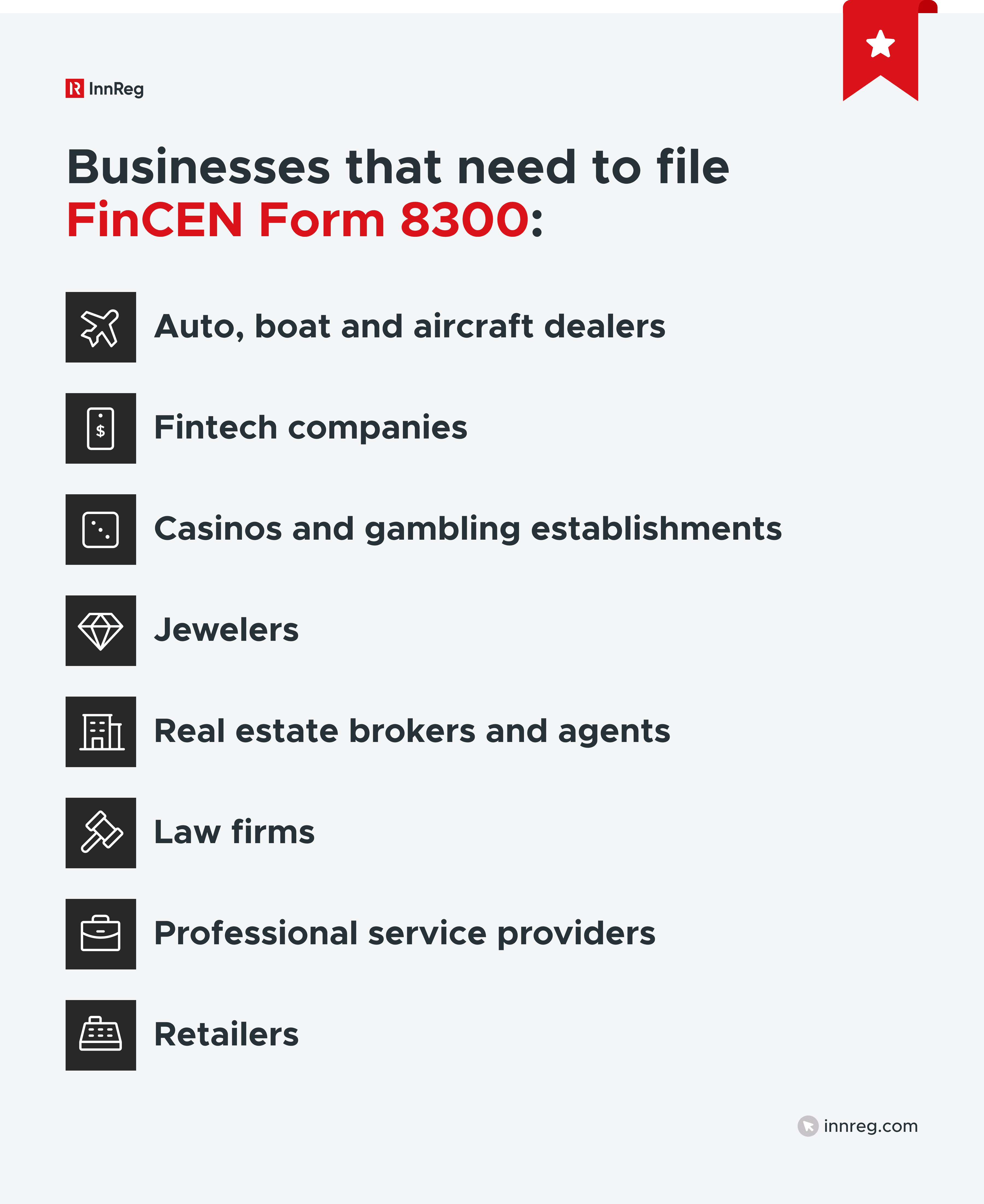

Who Must File FinCEN Form 8300?

Any person or business engaged in a trade or business may be required to file Form 8300. This rule applies broadly and is not limited to banks or financial institutions. If you accept more than $10,000 in cash in a single transaction or a series of related transactions, you fall under the filing obligation.

Businesses Covered

Form 8300 filing applies across industries. Businesses most often affected include:

Auto, boat, and aircraft dealers

Real estate brokers and agents

Jewelers, pawnbrokers, and high-value retailers

Casinos and gaming establishments

Law firms and professional service providers

Fintech companies that receive cash or cash equivalents through customer activity

The key factor is not the type of business, but whether your operations involve accepting large cash payments. For compliance officers, understanding when and how to file Form 8300 is a baseline requirement, even if cash transactions are rare in your business model.

When Filing Is Required

You must file a Form 8300 within 15 days of receiving more than $10,000 in cash. The rule applies whether the payment happens in a single transaction or multiple installments that are clearly related. If the 15th day falls on a weekend or holiday, the deadline moves to the next business day.

Filing is mandatory, not optional. Even one missed report can lead to financial penalties or heightened regulatory scrutiny.

Related Transactions and Structuring Rules

Payments are considered related transactions if:

They occur within a 24-hour period, or

They are part of a single deal or arrangement that you know is connected, even if spread out over longer than 24 hours.

For example, a customer pays $8,000 in cash on Monday and $3,000 in cash on Tuesday for the same purchase. This triggers a report. Or, a client makes a $5,000 cash down payment and another $6,000 in cash three months later toward the same contract. This also requires a filing.

Attempting to split payments to avoid reporting is called structuring. It is illegal and can carry both civil and criminal consequences for the business and the customer. Compliance teams should train staff to spot structuring attempts and treat them as red flags.

What Counts as “Cash” for Form 8300?

The term “cash” under Form 8300 has a specific definition. It is not limited to paper currency. Businesses must know what counts toward the $10,000 threshold to avoid missing a required filing.

Currency and Cash Equivalents

Cash does not always refer to physical notes of currency. Instead, when the term “cash” is used around FinCEN Form 8300, it means one of the following:

US and foreign coins and currency

Certain cashier’s checks, bank drafts, traveler’s checks, and money orders, if their face value is $10,000 or less, and are used in a designated reporting transaction

Multiple smaller instruments (for example, a $6,000 money order and $6,000 in currency for the same deal), if they push the total over $10,000

In practice, if your business receives more than $10,000 in combined cash and qualifying instruments, you must report it.

See also:

What Does Not Qualify as Cash

Some payment types do not count as cash for Form 8300 purposes. These include:

Personal checks drawn on the payer’s own account

Any transmittal of funds from a financial institution (i.e., Bank wires and ACH transfers)

Cashier’s checks, money orders, traveler’s checks, or bank drafts over $10,000 (since the bank reports those when issuing them)

For example, a $12,000 cashier’s check by itself is not treated as cash, but a $7,000 cashier’s check plus $5,000 in currency would be.

Need help with money transmitter compliance?

Fill out the form below and our experts will get back to you.

Special Rules for Foreign Currency and Monetary Instruments

Foreign currency is included if its value exceeds $10,000 when converted into US dollars. Businesses must calculate the fair market exchange rate at the time of the transaction.

Designated reporting transactions, such as retail sales of vehicles, jewelry, or collectibles, have additional rules for monetary instruments. In these cases, multiple small instruments may be treated as cash if used together in a high-value transaction. Compliance teams should document these payments carefully, as they are a common audit point.

How to File FinCEN Form 8300

Once a business receives more than $10,000 in cash, the countdown begins. Form 8300 must be filed within 15 days of the triggering payment. To stay compliant, companies need clear filing procedures, proper documentation, and internal checks.

Filing Deadlines

The 15-day clock starts the day the cash is received. If the due date falls on a weekend or federal holiday, the deadline moves to the next business day. Businesses that delay or miss this deadline risk penalties, even if the oversight was unintentional.

Electronic Filing vs. Paper Filing

There are two methods to file a FinCEN Form 8300. It can be filed through:

FinCEN’s BSA E-Filing System, which is the preferred method for faster processing and confirmation.

Paper filing by mailing to the IRS, available only for businesses not required to e-file.

As of 2024, businesses filing 10 or more information returns in a year must e-file Form 8300. For most fintech firms, electronic filing is now the default expectation.

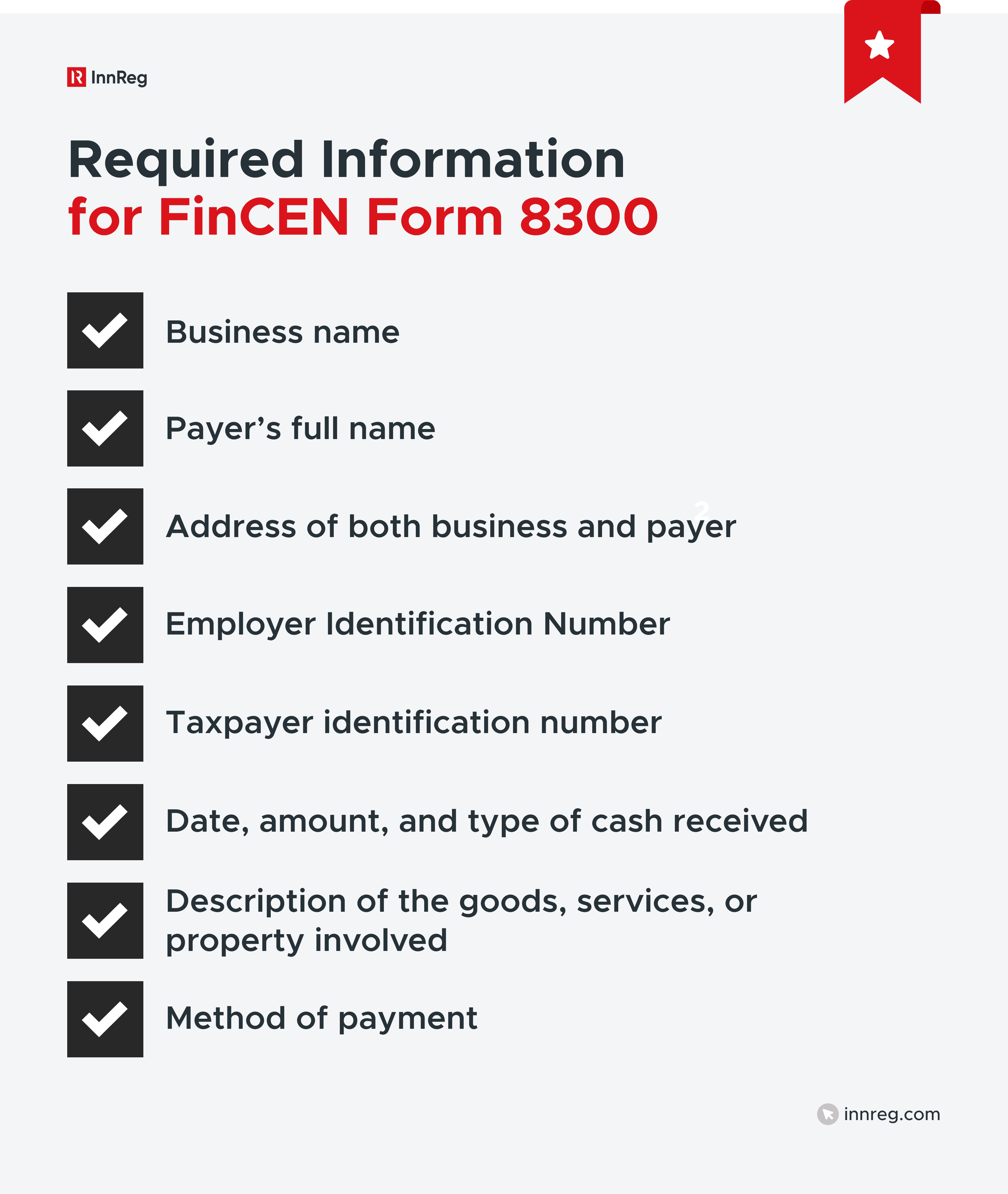

Required Information and Documentation

In order to successfully file a Form 8300, you need supporting information and documents. A complete filing includes the following details and documents:

Business name, address, and Employer Identification Number

Payer’s full name, address, and taxpayer identification number

Date, amount, and type of cash received

Description of the goods, services, or property involved

Method of payment (currency, cashier’s check, money order, etc.)

If the transaction appears suspicious, the form includes a comment section to add additional details to flag this for regulators. Incomplete or missing information weakens the filing and can draw scrutiny.

Customer Notification Requirements

Businesses must provide each payer listed on the form with a written statement by January 31 of the following year. The notice must include your business information, the amount received, and a note that you reported the transaction to the IRS.

This requirement helps promote transparency, but does not apply to voluntary filings made solely for suspicious activity.

See also:

Recordkeeping Obligations

Keep a copy of every Form 8300 and supporting documents for at least five years. That means holding onto receipts, ID records, and notes that explain how transactions were linked. Good recordkeeping isn’t just about checking a box. It helps your compliance team respond quickly if an audit or regulator inquiry comes up.

Common Compliance Challenges and Misconceptions

Filing FinCEN Form 8300 sounds straightforward, but many businesses struggle with the details. The most frequent problems come from gaps in monitoring, incomplete customer data, or misinterpreting what the rules require.

Tracking Multiple Payments and Aggregation

Businesses often miss filings because they look at payments individually instead of collectively. Related transactions must be added together to see if they cross the $10,000 threshold. A $6,000 cash payment followed by a $5,000 payment days later for the same deal is reportable. Without a tracking system, these links are easy to miss.

Collecting Customer Identification and Tax IDs

A complete Form 8300 requires the payer’s taxpayer identification number (TIN). Customers may hesitate to share it, but the law requires you to request it. An incomplete filing raises questions with regulators and may trigger penalties. Staff should be trained to explain why the information is needed and document any refusal.

Structuring Attempts and Suspicious Transactions

Some customers may try to avoid reporting by splitting payments. This practice, called structuring, is illegal. Accepting or ignoring it puts your business at risk of civil and criminal liability. Train staff to watch for red flags, such as repeated payments just under $10,000 or customers who explicitly mention avoiding paperwork.

Misunderstanding Industry Coverage

Many entrepreneurs believe that Form 8300 only applies to banks or businesses that deal mainly in cash. That is incorrect. Any business that receives more than $10,000 in cash is covered.

Even fintech firms that primarily operate online may encounter cash transactions through customer onboarding, kiosks, or partnerships. Overlooking this requirement can create avoidable compliance problems.

Recent Updates to FinCEN Form 8300

The rules around FinCEN Form 8300 continue to evolve. Businesses that rely on outdated practices risk missing new compliance requirements. The most important changes involve electronic filing mandates, the treatment of digital assets, and regulators' focus on high-risk industries.

Electronic Filing Mandate (2024)

As of 2024, businesses filing 10 or more information returns in a year must e-file Form 8300 through the BSA E-Filing System. Paper filing is now limited to small-volume filers. For fintech firms, electronic submission is the default, and setting up internal processes around the online portal is no longer optional.

Digital Assets as “Cash” Under Section 6050I

Regulators are catching up to the digital economy. Congress expanded the definition of “cash” to include digital assets such as cryptocurrency, a significant shift for businesses that accept crypto payments. Although the change was set to take effect in 2024, the IRS has postponed enforcement until it releases formal regulations.

Even with the delay, compliance teams should start preparing now. Once the new crypto reporting requirements take effect, large cryptocurrency transactions will be treated like cash under Form 8300. That means Form 8300 cryptocurrency compliance will include tracking wallet addresses, converting transaction values to US dollars, and verifying customer identities as part of the filing process.

Penalties for Non-Compliance

Failing to file FinCEN Form 8300 on time, filing it with missing details, or ignoring the requirement altogether can lead to costly penalties. Regulators treat non-compliance as both a reporting failure and a potential sign of deeper weaknesses in a business’s AML program.

Civil Penalties

Civil fines apply even when violations are unintentional. Negligent or late filings often result in per-form penalties that can add up quickly for businesses handling frequent cash transactions.

The IRS adjusts these amounts regularly for inflation, but fines commonly range in the hundreds of dollars per missed or incorrect form. If the agency concludes that a business intentionally disregarded the law, the penalties can rise sharply, with no cap on total exposure.

See also:

Criminal Penalties

When violations involve willful conduct, regulators can pursue criminal charges. Structuring or deliberately failing to report cash payments is a federal offense.

Penalties may include substantial fines for the business and individuals, and in severe cases, prison sentences of up to five years. These consequences highlight why Form 8300 compliance must be treated as a core part of financial operations, not an afterthought.

Best Practices for Compliance Programs

Nobody wants to deal with penalties or paperwork stress. The best way to stay ahead is to build simple, reliable processes for handling FinCEN Form 8300 filings. When your reporting runs smoothly, you not only meet deadlines, you also keep your compliance program strong and audit-ready.

Here’s how to get there:

Practical Steps for Filing Accuracy

Monitor cash receipts in real time: Set up systems to immediately flag when a transaction exceeds the $10,000 threshold. This helps you capture reportable payments before they slip through the cracks.

Create a filing checklist: Standardize the filing process with a clear checklist that includes essential details like payer information, transaction descriptions, and payment methods.

File on time: Be diligent about the 15-day filing deadline. Set internal reminders for the filing team so that no form is missed, even during busy periods.

Staff Training and Internal Controls

Train employees regularly: Conduct training sessions on identifying large cash transactions and collecting the necessary information (e.g., TINs).

Establish a clear escalation process: If a staff member notices suspicious behavior or a structuring attempt, they should know exactly how to escalate the issue.

Run internal audits: Regularly auditing your compliance processes can help identify gaps or weaknesses before they develop into larger concerns.

Technology and Workflow Tools

Leverage e-filing tools: Use FinCEN’s BSA E-Filing System to submit forms quickly and securely. Setting up your team’s workflow around this system will help streamline filing and reduce errors.

Integrate compliance systems: Sync your payment platforms, CRM, and accounting software to automatically flag large transactions and keep your records up-to-date.

Use compliance management software: Tools like Asana or Trello can help track tasks and deadlines related to Form 8300 filing, making the process more organized and less prone to human error.

Form 8300 vs. Currency Transaction Report (CTR)

Both Form 8300 and the Currency Transaction Report (CTR) are essential for reporting large cash transactions, but they serve different purposes and apply to different situations. Here is a simple table to help differentiate when to file what:

Aspect | Form 8300 | Currency Transaction Report (CTR) |

|---|---|---|

Threshold | Over $10,000 in cash or cash equivalents | Over $10,000 in currency (USD) received in a single transaction |

Filing Party | Businesses of all types, including non-financial firms | Financial institutions (e.g., banks, MSBs) |

Filing Deadline | 15 days after receipt of cash | Within 15 days of the transaction |

Filed With | FinCEN and IRS | FinCEN |

Applies To | Any business receiving cash for goods or services | Financial institutions and money services businesses |

Report Includes | Customer details, payment type, goods/services involved | Customer details, transaction specifics, and financial institution details |

Key Takeaways

Compliance with FinCEN Form 8300 is a critical component of a robust AML program. Whether you're a fintech startup or a long-established business that handles large cash transactions, it’s essential to understand the filing requirements and deadlines. Doing so helps you avoid penalties and keeps your regulatory reputation in good standing.

By following best practices for monitoring, reporting, and documentation, businesses can meet regulatory requirements and avoid costly mistakes. If your business is navigating Form 8300 compliance and looking for expert support, InnReg specializes in fintech-specific regulatory compliance.

We can act as your outsourced compliance department, helping you streamline processes, meet reporting requirements, and stay aligned with regulatory changes. Reach out today to learn how we can help you simplify compliance for your fintech business.

Bruno is a Principal Compliance Officer at InnReg advising fintech clients across broker-dealer, RIA, and money transmitter verticals. He brings prior experience at Santander Brasil and Passfolio, with expertise in regulatory strategy, supervisory systems, and compliance execution. He holds FINRA Series 4, 7, 24, 63, and 99 licenses.

How Can InnReg Help?

InnReg is a global regulatory compliance and operations consulting team serving financial services companies since 2013.

We are especially effective at launching and scaling fintechs with innovative compliance strategies and delivering cost-effective managed services, assisted by proprietary regtech solutions.

If you need help with money transmitter compliance, reach out to our regulatory experts today:

Related Articles

Featured LinkedIn Posts